Solving the Future Income Dilemma for the Single Woman

Single women face many challenges, including planning for their future income and a successful retirement. Most single women recognize that their lives will be different when they retire. Most would agree they will need a guaranteed lifetime of income, an income they cannot outlive.

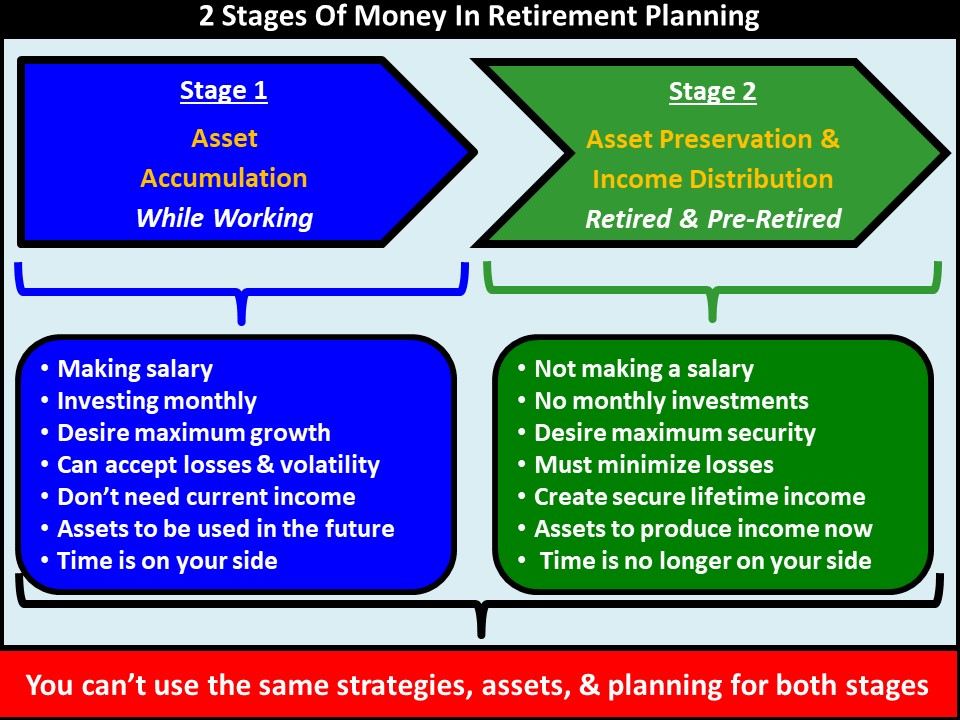

But Future Income Planning is Different

Most financial advisors and money gurus are focused on wealth accumulation and not the distribution of wealth. They are not wealth distribution experts. While accumulating wealth and saving for retirement were useful while you were working and earning an income when you retire, the rules of money change.

During the wealth accumulation phase, the stock market may have been a wonderful place to make a lot of money. For some people, it may still have a place in a wealth distribution mode. However, in retirement, your priority should be to avoid losing what you have earned while creating reliable retirement income.

Once you retire, it’s a totally different game

You’ve worked hard for the last 40 years, and you want to enjoy your retirement and have the standard of living that you’re used to. As soon as you stop saving and start spending, new risks come alive in your retirement, including:

- What if I live a long time?

- How will inflation affect my lifestyle?

- How much will I earn (or lose) on my retirement savings?

- What amount can I safely withdraw from my savings and not run out of money?

- How much will my health care cost rise over time?

- What is the impact of taxes on my future income?

You are no longer earning and saving money, you are distributing money that you saved, and it needs to last the rest of your life.

But the Challenge is

Many accumulation advisors may not consider all of these factors to help you plan for your retirement. And you may feel like they’re pushing investments on you. And then, it’s your job to fit the investments into your life and goals.

Some women feel that planning for future income is their responsibility.

If you have been in the market long enough, you know it has ups and downs. It can make and lose money. In a down market, your advisor is likely to tell you something like:

- “Don’t worry, ride it out; the market will come back.”

- “We will just keep investing the same way we always have and take money out as you need it.”

- “You must be in the market to have a successful retirement.”

And the dilemma is that in retirement, even when there are negative down years, you still need income.

A good distribution plan takes into account things like:

- Your age.

- When you plan to retire (or when you did retire).

- Your budget.

- When it’s best for you to take Social Security.

- Inflation adjustments.

- Required minimum distributions.

- Potential long-term care expenses.

- Your legacy goals.

- Your lifestyle.

- If you have a pension.

- Your risk tolerance.

- Your personal retirement lifestyle, dreams and goals, and much more.

What do you do to create a guaranteed future income?

If you ask fifty different financial professionals what the best way is to create a future income in retirement, you will get fifty different opinions. But there is only one optimal way, and that’s with a guaranteed lifetime income. It provides you with the best opportunity for retirement success.

Here is an Example:

Let’s take a look at an example of a woman who turned 60 this year. She is a single woman who plans to retire in six years with a projected Social Security income of $2,700 per month. There are no pensions or any other additional income sources available from any current or previous employer.

She has done an excellent job of accumulating wealth over her lifetime, and now she has $500,000 in a combination of an IRA and a Roth IRA. In six years, her broker assures her that they can take a future income of $2,500 off per month from her account until age 93. At age 93, the best guess is the $500,000 will be gone.

When she is retired, she would like to travel and enjoy her golden years. She wants to have ample income to cover her expenses and is comfortable with an additional $2,500 per month. One of her goals is to take her children to Disney World when she’s retired.

Maybe, Hope and Luck

The concern is that her current broker is basing her future income and retirement on hope and luck. Let’s hope the market performs as we expect, and if we’re lucky, we can make it to at least age 93. But she does not want to base her retirement on hope, luck, or a maybe when she retires in six years. She is looking for more of a sure thing.

The Concept: A Sure Thing versus a Maybe

She made a change to make sure that her retirement six years from now was going to be a sure thing rather than a maybe. She took $275,000 of her $500,000 and placed it into a Fixed Index Annuity with a lifetime income rider. By making this change today, she would be guaranteed by contract that even if the market were flat or went down, she would receive a future income of $2,500 per month for the rest of her life. Her income would not stop at age 93.

The only thing worse than dying is outliving your money

Also, she would still have $225,000 in her brokerage account that she could choose to spend or use as a hedge against inflation in the future. She could also apply some of those additional funds for guaranteed future income later in life. By making this change, she has leveraged a portion of her retirement savings to achieve her $2,500 monthly income goal. By transferring the risk of living too long to the insurance company, she now has a $225,000 cash reserve to meet unexpected bills and emergencies or to save or spend as she pleases.

Unlike in a bank or Wall Street, she did not need to chase an x% interest rate that is not guaranteed. She did not need to take risks with all her money.

While annuities aren’t for everyone, they can play a significant part in a stable and worry-free retirement. Fixed Index Annuities with an income rider offer two main benefits.

- Protected growth. You can share in the growth of a stock market index but not the losses.

- A steady and reliable paycheck for life now or in the future. This means you will receive a predetermined amount of income starting today or at some point in the future every month for as long as you live.

Both benefits can play a significant role in a happy and worry-free retirement. But retirement is primarily about income and cash flow, not how big of a stack of cash you have.

The Pro’s (Advantages)

Fixed Index Annuities with an Income rider are appropriate for you if you are searching for:

- Options to maximize your current and future income.

- Guaranteed lifetime income for one or two people.

- Guaranteed income for a specific time period for one or two people.

- Principal stability and guarantee.

- Access to your funds for income purposes.

- Guaranteed values to be paid to beneficiaries.

- Opportunity to earn a competitive rate of return based on a low-risk asset.

- Secure income-oriented asset with access to funds in case of long-term care needs.

The Con’s (Disadvantages)

Fixed Index Annuities with an Income rider are not appropriate for you if you:

- Do not require a planned Exit Strategy from your assets.

- Need 100% liquidity of your assets at all times.

- Do not desire guaranteed income from your assets now or in the future.

- Enjoy the thrill of risk-taking and feel principal stability and guarantees are not important.

- Are averse to fees.

- Do not want your funds to be subjected to surrender charges.

- Are not concerned about protecting asset values for beneficiaries.

- Are not worried about market volatility and principal loss do not worry you.

- Feel you must receive 100% of the upside on their assets regardless of the potential downside.

- Are under age 59½ and planning to take withdrawals from a fixed or fixed index annuity that could be subject to an additional 10% federal income tax penalty on any gain.

- Prefer not to have your income payments backed by the financial strength and claims-paying ability of an insurance company.

Caution: Guru’s Ahead

Many people have been led to believe that annuities are too complex and have high fees. Oftentimes, they hear this from financial gurus or advisors who are trying to sell them something else.

The key to finding out if an annuity is right for you is to talk to a financial professional specializing in income distribution. The ideal specialist has the knowledge and resources to shop, rate, compare, and recommend only the top annuity products from the top-rated insurance companies.

This is important

Remember that the income payments are backed by the financial strength and claims-paying ability of the insurance company or companies you chose. Therefore, it may be in your best interest to choose a highly rated insurance company or, better yet, multiple companies. You can check ratings from sources like AM Best, Fitch, Moody’s, and Standard and Poor’s.

In Conclusion

Having an annuity income rider on a fixed index annuity can provide you with an immediate or future lifetime of income you cannot outlive. You keep the right to use your cash value and maintain your safety of principal with interest paid on a tax-deferred basis. If you do not have a pension and want one, a lifetime income rider on an annuity could become your personal pension, private pension, or a do-it-yourself pension.

Finally

If you are at or near retirement and have any questions about how annuity income riders work on deferred fixed annuities or just need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

About Author Steven Drahozal

Steven has been in the financial services profession since 1986. He is a small business owner and runs a life insurance agency. Steve has been a part of the Mature American Planning Company, a Michigan Corporation and insurance agency, since its founding in 1998.

Steve also offers written goals-based retirement planning through the Wealth & Income Management Group, 425 W. Huron Street, Suite 220, Milford, MI 48381.

Investment advisory services offered through Brookstone Wealth Advisors, LLC (BWA), a registered investment advisor. BWA and Brookstone Capital Management, LLC are affiliated companies. BWA and the Wealth & Income Management Group are independent of each other. Insurance products and services are not offered through BWA.

Any comments regarding safe and secure products, and guaranteed income streams refer only to fixed insurance products. They do not refer, in any way to securities or investment advisory products. Fixed Insurance and Annuity product guarantees are subject to the claims‐paying ability of the issuing company and are not offered by Brookstone.

Index or fixed annuities are not designed for short-term investments and may be subject to caps, restrictions, fees, and surrender charges as described in the annuity contract. Guarantees are backed by the financial strength and claims paying ability of the issuer. Please refer to the BWA ADV 2A Item 4, for additional information.”