Is my Spirit Airlines 401(k) safe, and what should I do now that this permanent ground stop forced me to make an emergency retirement landing?

As a pilot, flight attendant, ground crew, ground staff, or other personnel, you may not have been planning to make an emergency retirement landing from Spirit Airlines. But it happened. And you might be wondering, is my Spirit Airlines 401(k) safe? Yes, it is. But Spirit Airlines is closed. Now what?

The good news is you have free time on your hands to research your 401(k) rollover opportunities and to find out if you can retire early. The bad news, of course, is you’re out of the job, possibly a few years sooner than you may have been planning, and your 401(k) assets are temporarily frozen. What’s the next move for your retirement?

Riding the slide off to your emergency retirement landing

For many, and maybe for you, retirement was supposed to be a few years down the road, not now. You weren’t planning on retiring at this point in your life. Your Spirit Airlines 401(k) hasn’t yet hit what you believe is the “magic number,” the right amount of money in your retirement plan, so you can enjoy your happily ever after. Unfortunately, due to higher fuel prices and a number of other reasons, Spirit is no longer in business.

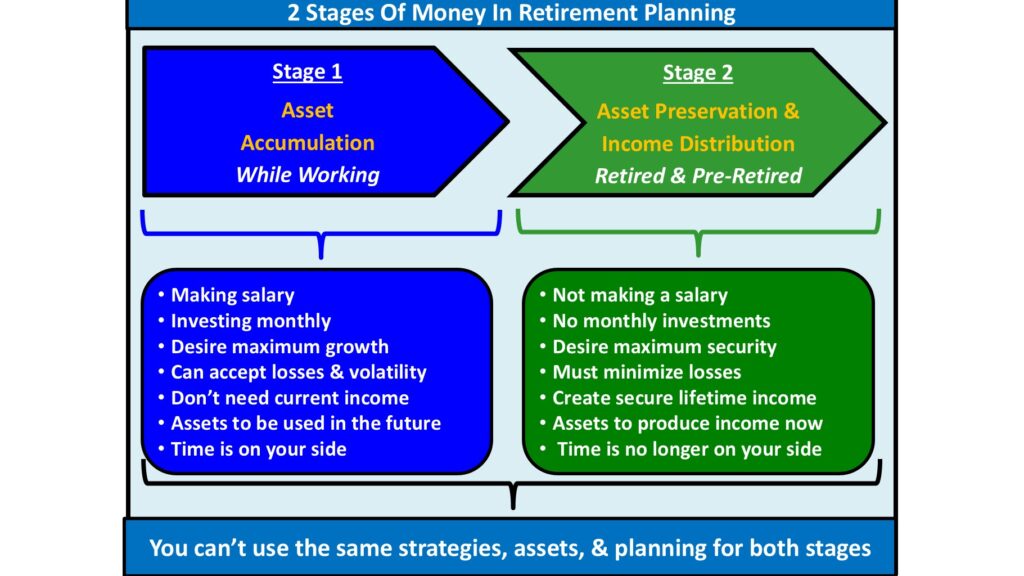

While you were working, the Spirit Airlines 401(k) was an excellent tool for the “climb” of accumulating retirement wealth. It helped you save and accumulate a great deal of assets while you caught the Spirit and traveled your way. But now that you have abruptly landed, you are no longer receiving a paycheck. You are no longer contributing to your 401(k). Time is no longer on your side. You might want to retire, but can you?

This cloud may have a silver lining

Currently, if you are considering retiring, you will find that today’s retirement plans have income payout rates and guarantees that are at an all-time high. Even though you may have arrived at your destination earlier than you expected, you may be able to make this your final flight and enjoy a happily ever after.

Small Changes, Big Results

You’d be surprised how many people come to my office who don’t think they can retire early but have all the assets they need. They just have their wealth allocated incorrectly. Sometimes, making a few changes, you can retire now, not years from now. By repositioning your assets, you may be able to retire now as well. All you might need is a proper rollover and allocation of your Spirit 401(k).

The Retirement Secret

Many people think they need between $1,000,000 and $2,000,000, or more, in assets to live on for the rest of their lives. Assets are not income. A success in retirement is not based on the size of your pile of money. It is based on the distribution of wealth from that pile. It is about having enough guaranteed income coming in to support your ideal lifestyle for as long as you live.

Risk is for people trying to get you the money that you already have. All you have to do is not lose.

You can have a lot of money and still feel financially insecure. Why? Because security doesn’t come from account balances. It comes from knowing your income will last, your expenses are covered, and your future is protected. Some retirees with large portfolios still worry every month. Others with structured income feel confident, relaxed, stress-free, and worry-free. Security isn’t about how much you have. It’s about how reliably it supports your life.

Why delay retirement when you can afford it?

A lot of people could retire, but don’t. Not because they don’t have enough money, but because they’re not sure what their income will look like. When you’re working, income is predictable. But sometimes in retirement, Wall Street can make it unpredictable. This creates income insecurity. If you don’t know what your income looks like in retirement, you need to understand it before you embark on your retirement journey.

One of your biggest challenges

If you ask 50 different advisors, they’re going to give you 50 different opinions on what the right way to retire is. There’s only one optimal way to retire, and that’s to have a guaranteed income to cover your lifestyle and all expenses. You need to plan for the worst and hope for the best. You need to separate your lifestyle from your investment strategy. The best plans are based on math and science, not opinion, hope, and luck.

Conventional Wisdom:

If you talk to your typical broker, they may offer you their opinion. Most likely, the suggestion will be to set you up with a diversified portfolio based on your risk tolerance that might look like:

• 30% Stocks, 70% Bonds

• 40% Stocks, 60% Bonds

• 50% Stocks, 50% Bonds

• 60% Stocks, 40% Bonds

• 70% Stocks, 30% Bonds

Then the plan will be to withdraw 4% from the portfolio, and then you have a 90% to 95% chance that your income will last your lifetime.

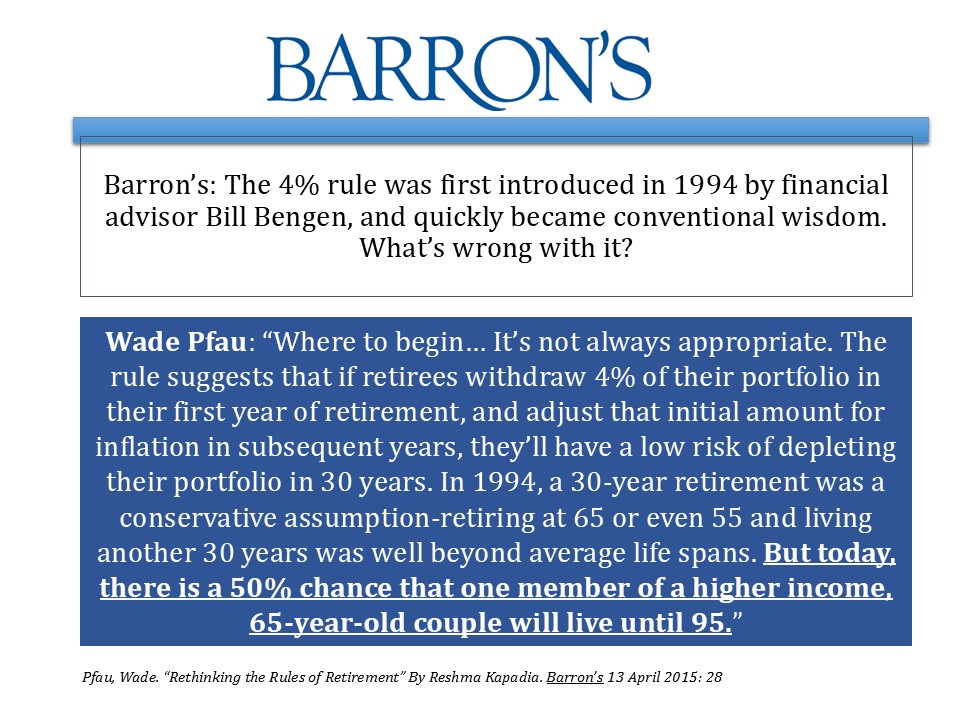

The Birth of the 4% Safe Withdrawal Rate

In October 1994, financial planner William Bengen published a paper, “Determining Withdrawal Rates Using Historical Data”, in the Journal of Financial Planning. This groundbreaking research used historical market data to test various withdrawal rates across all rolling 30-year periods since 1926. He concluded that a retiree could withdraw 4% of their initial portfolio balance, adjusted annually for inflation, and reliably sustain income for at least 30 years, even through the worst market conditions.

You could outlive your income

Bengan found that 4% might work for the first year of retirement, but should be adjusted in subsequent years. While the rule is fairly simple to apply, many failed to apply it appropriately. In the event of a prolonged period of low interest rates, combined with a 4% withdrawal rate, this combination could cause the underlying portfolio to drop to zero. If you had $1,000,000, and you withdrew 4%, you could have $40,000 of income.

Ask yourself: if you’re on a plane about to bound for a Caribbean vacation, and just before takeoff, the pilot says, “It’ll be a 3-hour flight, when we land it’ll be sunny and 78 degrees with a slight breeze of 3-5 miles per hour. We want to thank you for flying with us, and today there is only at 10% chance we crash.” Do you stay on that flight?

You probably want a sure thing, not a maybe

I don’t know about you, but I wouldn’t be flying Spirit Airlines if my flight had about a 90% chance or less) of making it to its final destination. In its 34-year history, Spirit has never had a fatal passenger crash. In your retirement, you should expect the same result. You deserve a 100% chance of making it through your golden years. Plan for the worst and hope for the best.

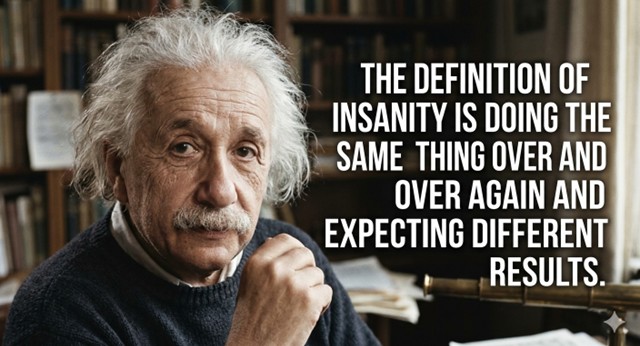

Albert Einstein is credited with the quote about the definition of insanity: “Doing the same thing over and over again yet expecting different results.” When time is no longer on your side, you are not earning a salary, and are no longer contributing to your 401(k), why would you continue to invest as though you are still accumulating assets? At this point in your life, you should probably focus on preserving wealth and distributing it to create a reliable income.

Get an Income for Life Analysis

One of the best tools to help people retire now is the Income For Life analysis. The focus is on income, not exclusively growth or assets. When creating an Income for Life report, your financial professional should consider things like:

• Social Security.

• Pension Information.

• Retirement plans like, 401(k)s, IRAs, Roth IRAs, 403(b)s, TSPs, etc.

• non-IRA account statements.

• Your lifestyle.

• Your monthly spend.

• Inflation.

• Your income cliff.

The goal should be for you to see your retirement income laid out in an easy-to-read (and understand) format. This simple and easy-to-understand format makes it so clear (and simple) as to where your income is likely to come from during your retirement.

Properly prepared, an Income For Life analysis will start to answer the questions you have about where your income will likely come from in your retirement. What you want to know is what your income’s going to be each year for the rest of your life. That way, you can determine whether you can retire and when.

How safe is my Spirit Airlines 401(k)?

Shortly after Spirit Airlines’ operational shutdown on May 2, 2026, your Spirit Airlines 401(k) plans began a transition to a court-appointed trustee. This created a 401(k) blackout period. Much like a very long flight delay, you will have limited or no access to your retirement funds for several weeks or months. While this is what is happening:

• A trustee will take over the administration of Spirit’s 401(k) plans to manage the assets.

• Your 401(k) plan assets will be held in a separate trust with a third-party custodian and be shielded from Spirit’s creditors, even during bankruptcy.

• Spirit has announced that all previously unvested employer contributions are now fully vested.

• The 401(k) plans will likely be terminated, allowing you to roll over your accounts into a new employer-sponsored retirement plan or an IRA, or take them as cash.

The Next Best Move

Now is the time to be talking to a financial professional about the money you have at Spirit. If you know you are not ready to retire, talk to a financial professional about how best to accumulate wealth. If you are at or near retirement, talk to a financial professional who specializes in wealth distribution. Find out what it is going to take to get to that lifestyle you are dreaming about. You may have encountered some turbulence in your trip, but you don’t have to let a retirement emergency landing create a diversion from your goals.

When the blackout period ends, and you have access to your Spirit Airlines 401(k) assets, your choices will most likely include:

• Rollover to an IRA: Transferring your savings to an Individual Retirement Account is a sound strategy to help avoid paying taxes and penalties. A change could open up a wide range of ways to handle your assets that may not have been available in your 401(k). You can maintain control of your retirement savings.

• Transfer to a New Employer’s Plan: If you become an experienced hire elsewhere and start a new position that includes a retirement plan, you could transfer your previous savings to the plan at your new employer. The control of your transferred retirement savings will most likely be subject to the rules of your new plan.

• Cashing Out: Withdrawing your funds is generally not advised. There is a 20% tax withholding requirement and significant tax implications and potential penalties for early withdrawal.

In whatever you decide to do, you need to understand the pros and cons. If you are looking into retirement now or in the near future, you want to talk to a distribution specialist. A distribution specialist is a financial professional who can help you create an income you cannot outlive. It may not be the same person who has helped you accumulate your assets while you were working. Don’t accept a pie-in-the-sky retirement. Select a retirement for what it will do, not what it might do.

The Bottom Line

If you are at or within a few years of retirement before Spirit forced you into an emergency retirement landing, you may still be able to retire. You may have all the assets that you need to retire on in your Spirit Airlines 401(k), but they are just allocated incorrectly. Conventional wisdom and a large stack of cash may not be the best way to live happily ever after with an income you cannot outlive. A financial professional who specializes in the distribution of assets can help you figure out if you are in a position to retire now and enjoy the lifestyle of your dreams. So, grab your flight records. It’s time to disembark and slide into your retirement from Spirit.

– – – – – – – – – – – – – – – – – – – – – – – – –

About Author Steven Drahozal

Steven has been in the financial services profession since 1986. He specializes in the distribution of assets for people at or near retirement. He is a small business owner of the Wealth & Income Management Group, LLC, and runs a life insurance agency. Steve has been a part of the Mature American Planning Company, a Michigan Corporation and insurance agency, since its founding in 1998. He can be reached at steven@retirewithwimg.com or (810) 626-5101.

Investment advisory services offered through Brookstone Capital Management, LLC (BCM), a registered investment advisor. BCM, the Wealth & Income Management Group, LLC, and the Mature American Planning Company are independent of each other. Insurance products and services are not offered through BCM but are offered and sold through individually licensed and appointed agents.

Any comments regarding safe income and secure products, and guaranteed income streams refer only to fixed insurance products. They do not refer, in any way, to securities or investment advisory products. Fixed insurance and annuity product guarantees are subject to the issuing company’s claims-paying ability and are not offered by Brookstone.